BLOCKCHAIN Tutorial

Last updated on 19th Sep 2020, Blockchain, Blog, Tutorials

What is Blockchain?

Blockchain is a secure series or chain of timestamped records stored in a database that a group of users manages who are a part of a decentralized network. Blockchain is a decentralized or distributed ledger where each node in the network has access to the data or records stored in a blockchain. The encryption of all the important data records in the blockchain is done using cryptographic techniques. This ensures the security of the data in the blockchain.

So, the primary concept behind blockchain technology is having a network of multiple users or computers known as “Nodes” which can have secure and legitimate transactions directly without a third-party mediator. Any authorized node that is a part of the network can access the set of records added as a legitimate block in the blockchain. This makes the blockchain system an immutable, distributed digital public ledger that can record financial as well as other types of transactions. In the sections to follow, we will learn in detail how blockchain work but before that let’s check the history of technology in the blockchain tutorial.

Why Blockchain?

As we have seen, there is absolutely no central control, no national boundary, and no specific owner in Blockchain. Its security is powered by sophisticated cryptographic processes performed by p2p users, through a process known as mining.Here are some of the reasons why we need to embrace Blockchain technology.

- Secure – It is impossible for anyone to tamper with transactions or ledger records present in Blockchain.

- Worldwide Adaptation – Blockchain has been adopted worldwide and has the backing of many investors from both the banking and non-banking sectors.

- Automated Operations – In Blockchain networks, operations are fully automated through software implications. Private companies are not needed to oversee the operations.

- Open-source Technology – Blockchain happens to be an open-source technology. All operations within a Blockchain network are carried out by the open-source community.

- Distributed Architecture – Blockchain works in a distributed mode in which records are stored in all nodes in the network. If one node goes down, it doesn’t impact the other nodes or records.

- Flexible – The Blockchain network can be programmed using the basic programming concepts. This flexibility makes Blockchain networks easy to operate on.

Blockchain History

Stuart Haber and W. Scott Stornetta introduced the concept of a secured chain of blocks (set of records) in 1991. Later in 2008, a person or a group known by the pseudonym “Satoshi Nakamoto” conceptualized and implemented the blockchain technology. They introduced the concept of using hashing in the blockchain system to make it so secure that no one can make changes or remove the records once saved in the blockchain. The Bitcoin cryptocurrency system uses this blockchain design as its fundamental or base technology.

Prerequisites to Learn Blockchain

The main prerequisite to learn blockchain technology and make it a full-time thing is to have a solid technical background and thorough knowledge of the blockchain. The technical skills you need to be good at before starting professional work with blockchain are:

- Software development practices

- Data analytics

- Vulnerability analysis

- Traditional as well as advanced analytics

- Cryptography

- Embedded programming

- Comprehensive testing

Types of Blockchain

There are primarily two types of blockchains; Private and Public blockchain. However, there is a third type of blockchain too, known as Consortium blockchain. Before we get into details of the different types of blockchains, let us first learn what similarities do they share. Every blockchain consists of a cluster of nodes functioning as a peer-to-peer (P2P) network system. Every node in a network has a copy of the ledger which gets updated timely. Each node on all types of blockchain can verify transactions, initiate or receive transactions and create blocks.

Now in the blockchain tutorial, let’s have a look in detail about the three types of blockchains that are possible.

- 1. Public Blockchain: A public blockchain is a non-restrictive, permission-less distributed ledger system. Anyone who has access to the internet can sign in on a blockchain platform to become an authorized node and be a part of the blockchain network. A node or user which is a part of the public blockchain is authorized to access current and past records, verify transactions or do proof-of-work for an incoming block (thus, do mining). We use public blockchains for mining and exchanging cryptocurrencies thus, the most common public blockchains are Bitcoin and Litecoin blockchains. Public blockchains are mostly secure if we follow security rules and methods strictly. Although, it is only risky when the participants don’t follow the security protocols sincerely.

- 2. Private Blockchain: A private blockchain is a restrictive or permissioned blockchain operative only in a closed network. Private blockchains are usually used within an organization or enterprise where only selected members are participants of the blockchain network. The level of security, authorizations, permissions, accessibility is in the hands of the organization. So, we use private blockchains for similar purposes as a public blockchain but have a small and restrictive network. Examples of private blockchains are; Multichain and Hyperledger projects (Fabric, Sawtooth).

- 3. Consortium Blockchain: A consortium blockchain is a semi-decentralized type where more than one organization manages the blockchain. Contrary to what we saw in a private blockchain which a single organization controls. Thus, in a consortium blockchain, more than one organization or authority manages the blockchain. More than one organization can act as a node in this type of blockchain and exchange information or do mining. Examples of consortium blockchain are Energy Web Foundation, R3, etc.

Subscribe For Free Demo

Error: Contact form not found.

Working of Blockchain

Now, let’s come to the most interesting part of the blockchain tutorial that is how does blockchain work? By far, we have learned that blockchain is a concept of a decentralized network and distributed digital ledger. In this ledger system, legitimate and secure transactions can take place as a point-to-point exchange. So, let us understand the working of this technology and how it is used to record information and carry out secure transactions.

Blockchain is a system of network of multiple nodes or computers which acts as a distributed network over the internet, worldwide. Each node has the authority to make a transaction, verify a transaction, receive a transaction and create a block. The blockchain is a cryptographically linked chain of blocks (set of records) such that no one can falsify or modify the data stored in it. Once we enter a set of transactions in a blockchain then it becomes a part of it forever. So, we can call blockchain to be a distributed database whose data is unchangeable. Each node on a blockchain network has a separate copy of this ledger or database. They can access the transaction history on the blockchain whenever they want and get it updated every time a node adds a set of new transactions (block) into the chain.

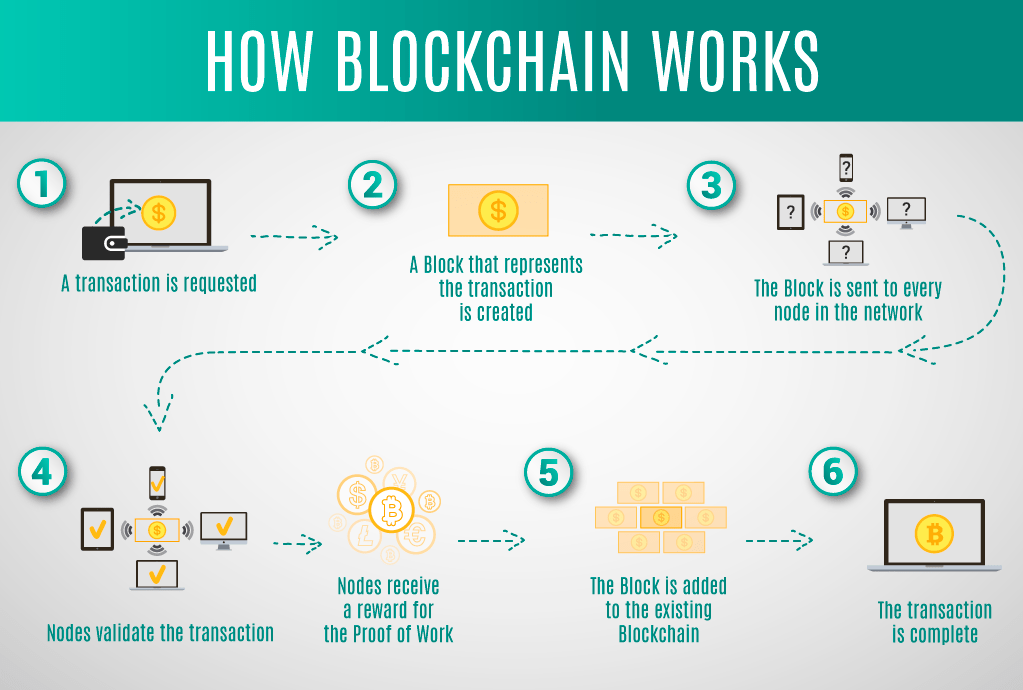

We will now understand the entire process by dividing it into individual steps.

Step 1: Suppose, two nodes in a blockchain network say node A and node B wants to make a new transaction.

Step 2: This transaction can only take place if all the other participant nodes in the network verify it as a legitimate transaction. Thus, each node will receive the request to verify the transaction to happen between A and B.

Step 3: Each node will check certain points about the transaction such as the authenticity of the two nodes, is the transaction amount within limits, does A have sufficient funds to make this transaction, etc.

Step 4: Once all the nodes check and verify all the aforementioned points, the transaction is ready to take place. Then that transaction gets added into a memory pool or mem pool.

Step 5: Several such verified transactions get aggregated into mem pools and multiple mem pools combine together to make a block. Every block has a defined memory limit to store transactions.

Step 6: Every new block will have a block header, that consists of transaction data summary, timestamp, hash code of the previous block and its own hash. Every block has its unique hash code which acts like its fingerprint.

Step 7: In order to add a new block into the existing blockchain, nodes in the network need to do proof-of-work. As we know, each block has its unique hash function which is an identification code created using SHA256. Doing proof-of-work is decrypting this code and finding the correct answer to this hash puzzle. To do proof-of-work, we need specialized computers that take on an average of 10 minutes to crack the code automatically.

Step 8: A block gets verified every time a node completes its proof-of-work and finds the correct answer to the hash puzzle for that block. More and more nodes must verify or complete the proof-of-work for the same block so that it finally gets added into the blockchain. Every block has a unique set of transaction records. To create a new block and add it to the blockchain, one must have a completely unique set of transactions in that.

Step 9: With this, a new block gets added and a transaction is completed between points A and B.

This process repeats itself and new blocks continue to get added in the blockchain permanently. There is a unique concept of rewards upon doing proof-of-work which we will learn in the lessons to come.

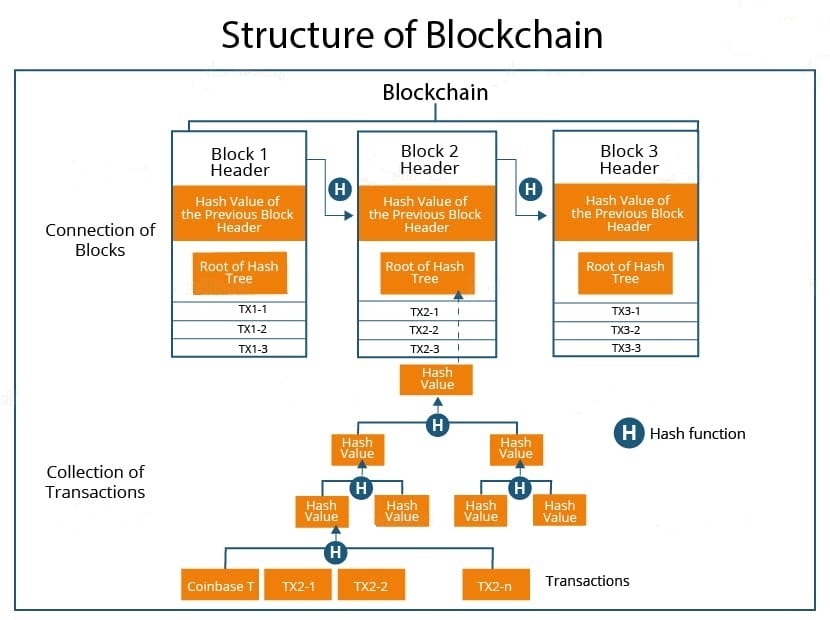

BLOCKCHAIN ARCHITECTURE

When we investigate the DNA of blockchain architecture for a better understanding, we need to analyze several aspects that contribute to this disruptive technological marvel. How does blockchain work? These aspects include the blockchain platform, nodes, transactions that make blocks, security implementations, and the process of adding new blocks to the chain. The blockchain architecture is undoubtedly complex, but once you get a hold of it you will get acquainted with the same.

Blockchain Diagram: Here’s a basic architectural representation of a blockchain.

With blocks being connected with each other through their respective hash codes, the whole blockchain ecosystem becomes a Fort Knox technically. Whenever a blockchain transaction flag is raised, a blockchain consensus needs to be achieved to update the same in the blockchain. Instead of relying on a third party to mediate transactions, member nodes in the blockchain network stick to a blockchain consensus protocol to agree on the ledger content and cryptographic hashes and digital signatures to ensure the integrity of transactions. Once authenticated, these blockchain transactions are considered successful and irreversible. Transactions rely a lot on hash values and hash functions. These hash functions are mathematical processes that take input data of any size, perform required operations on it, and return the output data of a fixed size. These functions can be used to take a string of any length as input and return a sequence of letters of a fixed length. This functionality of hash functions makes them apt for transaction processing. Regardless of the size of transactions, the final output will always be fixed and untampered.

After coming across the term ‘hashing’ these many times, it has become a matter of innate necessity for us to understand what hashing depicts. Also, let’s shed some light on the ‘identity’ of blocks.

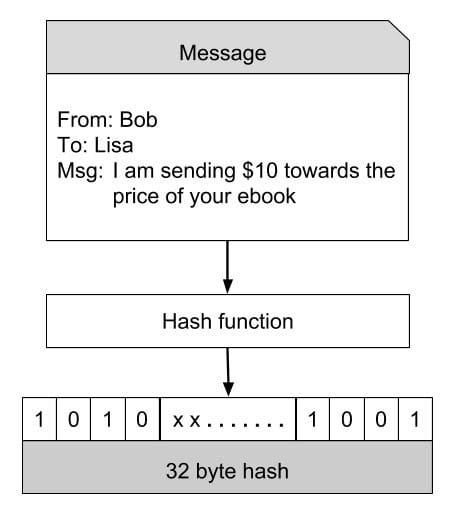

Under the hood of blockchains, hashing is necessarily a process that helps differentiate between blocks. The process of hashing gives blocks in a blockchain a unique identity. Technically, blocks in a blockchain are identified by their hash, which serves the purposes of both identification and integrity verification. An identification string that also provides its own integrity is called a self-certifying identifier. The hashing functions generate public keys. Here’s an example pertaining to hashing for a bitcoin blockchain.

Bitcoin uses SHA-256 hash function that produces a hash code of size 256 bits or 32 bytes.

Blockchain Diagram: Bob, while placing an order with Lisa, creates a message which is like the one shown above. This message is hashed through a hash function that produces a 32 bytes hash code. The beauty of the hash is that for all practical purposes it can be considered unique for the contents of the message. If the message is modified, the hash value will change. This makes it impossible to reconstruct the original message. Hacking, therefore, is a distant dream with hash functions.

Cryptographic Keys and Digital Signatures

As the information on the blockchain is transferred over peer-to-peer (P2P) networks across the globe, cryptographic keys are incorporated to send data throughout the network without compromising the safety and integrity. These keys not only allow blockchains to respect the privacy of users but also uphold the ownership of assets and secure the information of blocks in the network. Cryptography is applied throughout the entire blockchain onto all the information that is stored and transacted. This provides users with cryptographic proof that serves as the basis for trusting the legitimacy of a user’s claim to an asset on the blockchain. Cryptographic hashes also help a great deal as they ensure that even the smallest change to a transaction will result in a different hash value being computed, which will eventually indicate a clear change in the transactional history.

While cryptographic keys are necessary for safety and integrity, digital signatures provide verification and authentication of ownership on the blockchain. Using cryptographic digital signatures, a user can sign a transaction proving the ownership of that asset and anyone on the blockchain can digitally verify the identity to be true.

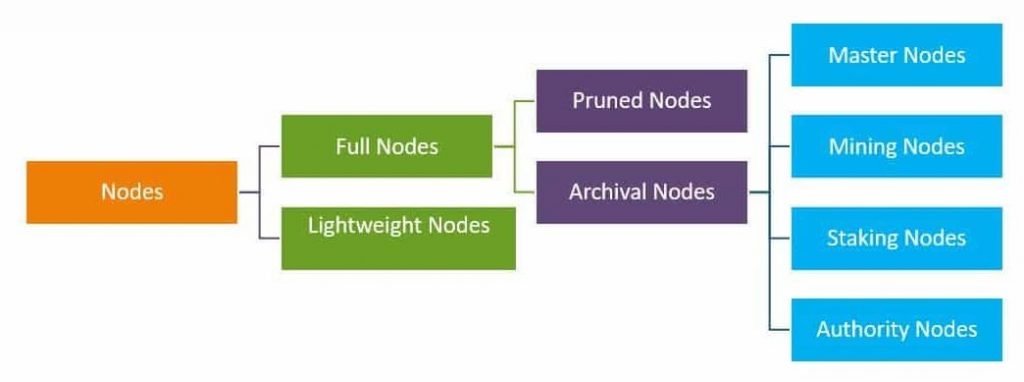

Blockchain Nodes

In simple terms, every participant in a blockchain network is a node. Being a decentralized network where a central authority is absent, there is great value for blockchain nodes. There exist several types of blockchain nodes, and each of them requires specific hardware configurations to get hosted or connected. Basically, there are two types of nodes: full nodes and lightweight nodes. These types comprise a constellation of a variety of nodes that are grouped under them.

Full nodes: act as a server in a decentralized network. Their main tasks include maintaining the consensus between other nodes and verifying the transactions. They also store a copy of the blockchain, thus being able to securely enable custom functions such as instant send and private transactions. When making decisions for the future of a network, full nodes are the ones that vote on proposals.

Pruned Full Nodes: The specific characteristic here is that these nodes begin to download blocks from the beginning, and once they reach the set limit, the oldest ones are deleted, retaining only their headers and chain placement.

Archival Full Nodes: These are what most people refer to when they talk about full nodes. These nodes envision a server that hosts the full Blockchain in its database.

Compared to full nodes, Master nodes themselves cannot add blocks to the blockchain. Their only purpose is to keep a record of transactions and validate them. Whether Mining or Staking nodes, they’re the ones who write blocks on the blockchain.

Lightweight or Simple Payment Verification (SPV) nodes, on the other hand, are used in day-to-day cryptocurrency operations. These nodes communicate with the blockchain while relying on full nodes to provide them with necessary sets of information. They do not store a copy of the blockchain but only query the current status for the last block. Also, they broadcast transactions to other nodes in the network for processing.

Get Blockchain Training with Advanced Topics From Real-Time Experts

- Instructor-led Sessions

- Real-life Case Studies

- Assignments

Blockchain Consensus

In the previous section, we got to know about the consensus. What does this term mean? The set of rules by which a blockchain network operates and validates the information of blocks is known as ‘consensus’.

Since cryptocurrencies operate on a decentralized P2P network, it won’t be wrong to assume that complications are bound to arise when a decision needs to be taken. This is where consensus comes in handy. While consensus must be achieved by a certain type of nodes, in P2P networks any user can become a full node and thus gain supremacy over others. When at least 51% nodes agree on something, the decision is validated on behalf of the whole of the blockchain. This 51% rule may result in threats even. The most common threat to a blockchain is the 51% attack, where more than half of nodes are concentrated in one entity. This paves the way for the entity to change consensus rules as it sees fit, which could lead to a monopoly.

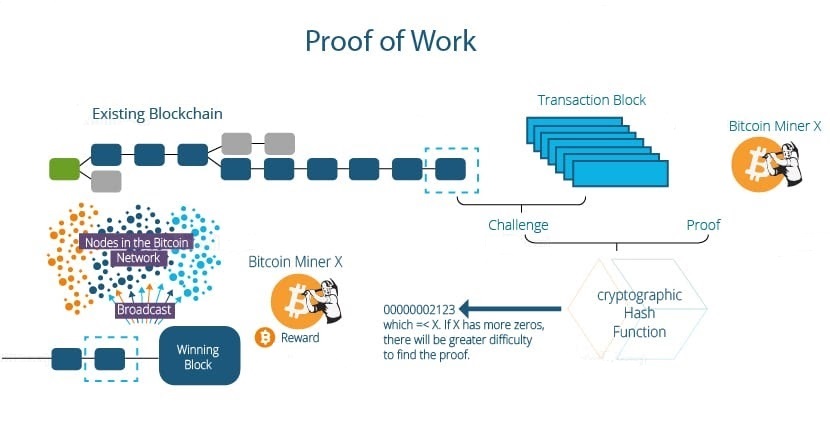

Blockchain proof of Work

A popular consensus mechanism for blockchains, Proof of Work is a requirement through which expensive computations, also called mining, can be performed in order to facilitate transactions on the blockchain. Although it might be hard for nodes to generate a valid block, it is quite easy for the network to validate the block’s authenticity. This is achieved through hash functions. Since hashes are quite sensitive to changes and even minute modifications will result in a completely different hash output, they can be used to validate and secure blocks.

For a block to be confirmed as valid, miners are required to generate two hashes: a hash of all the transactions in the block and one proving that they have expended the energy required to generate the block by solving a special cryptographic puzzle with a pre-set level of difficulty. The difficulty of solving the puzzle can be automatically adjusted in Proof of Work systems to create a consistent time period for blocks that are to be added to the blockchain.

In summary, a miner creates a block of valid transactions. Further, the miner runs a Proof of Work algorithm on it to find a valid hash. When a valid block is generated, the block is added to the blockchain, and the miner receives network fees and the newly created cryptocurrency.

Blockchain Protocols

As blockchains are being rolled out at an exponential rate for everything from cross-border financial transactions to supply chain management, the lack of scalability has remained a constant issue since the genesis of blockchains. As more computers join the P2P network, the efficiency of the whole blockchain ecosystem typically deteriorates. Through the process of sharding, a way of partitioning, blockchain miners can maintain a consistent throughput throughout the network.

Blockchain protocols, however, demand constant attention for their efficient functioning.

Block Chain Protocol Characteristics

- Each party maintains its own copy of the information, and all nodes must validate updates collectively.

- The information could represent transactions, contracts, assets, identities, or practically anything else that can be described in digital form.

- Entries are permanent, transparent and searchable, which make it possible for community members to view transaction histories in their entirety.

- Each update is a new block added to the end of a chain. A protocol manages how new edits or entries are initiated, validated, recorded, and distributed.

- Cryptology replaces third-party intermediaries as the keeper of trust, with all blockchain participants running complex algorithms to certify the integrity of the whole.

Major blockchain protocols are listed below:

- 1. Bitcoin: The first application of blockchains, Bitcoin enables users to perform non-reversible transactions trustlessly. This protocol includes technologies such as hash, digital signature, public-key cryptography, P2P networking, Proof of Work and Proof of Work mining.

- 2. Ethereum: Known for smart contracts, Ethereum features a native cryptocurrency, namely Ether, and an Ethereum wallet. This protocol allows users to create decentralized applications and democratic autonomous organizations.

- 3. Ripple: Ripple supports tokens that are used to represent fiat, other cryptocurrencies, commodities, or other value units such as mobile minutes and frequent flyer miles.

- 4. Hyperledger: Developed by the Linux Foundation in 2015, Hyperledger supports Python, endorsement policies for transactions and confidential channels for private information sharing.

- 5. Openchain: A scalable and secure blockchain protocol, Openchain is suitable for organizations that wish to issue and manage their digital assets.

- 6. IOTA: Known for its blockless distribution ledger ‘Tangle’, IOTA enables infinitesimally small payments without charging extra fees.

- 7. Lisk: A relatively new blockchain protocol, Lisk allows the development of decentralized applications in pure JavaScript.

- 8. BigchainDB: This open-source system starts with a big data distributed database and then adds blockchain characteristics to the network including decentralized control and digital asset transfers.

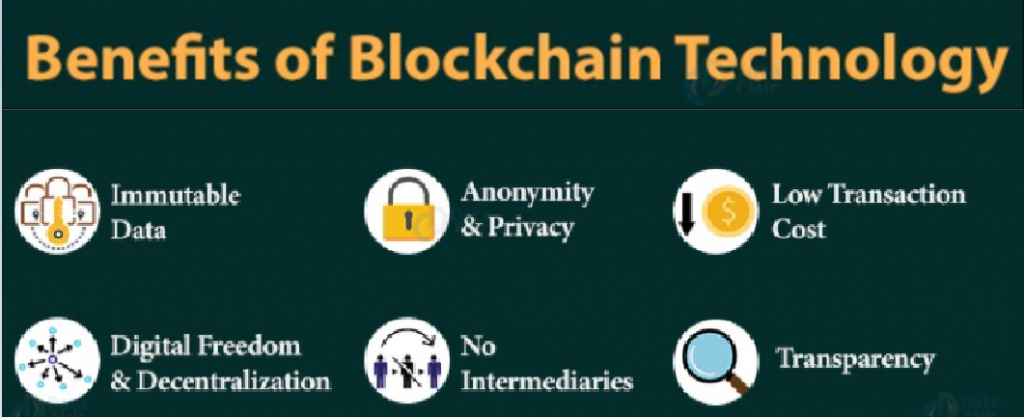

Benefits of Blockchain Technology

Blockchain technology is a revolutionary technology if accepted and implemented properly. It is a direct and secure way of conducting financial transactions or exchange files within a network.

Here are some major advantages of the blockchain technology that makes it so unique and popular.

- Immutable data: One cannot change a data record or information that is once stored or added as a block in the blockchain. The data in the blockchain is immutable, that is no one can make changes in it and it gets a permanent place in the blockchain.

- Digital freedom and decentralization: The entire blockchain network is a decentralized one as it gives every user its digital freedom. There is no central authority that controls all the other users in the network. Every node is independent in functioning.

- Anonymity and privacy: The blockchain network has tight security techniques for the transactions to take place securely. For users that use blockchain for cryptocurrencies like Bitcoin, can do so anonymously (without revealing their real identity) keeping their privacy and security ensured.

- Security: The security method in the blockchain is cryptography that ensures that hackers cannot change or tamper with the data records stored in the blocks of the blockchain. Encrypted hash functions link all the blocks in the blockchain and so it is impossible to do fraud or illegitimate transactions in the blockchain network.

- No intermediaries: Due to the point-to-point nature of the blockchain network, transactions take place directly between two nodes without a mediator. There is no need for an intermediary like Paypal, any bank, Visa, WesternUnion, etc. to facilitate transactions between two parties.

- Transparency: The digital distributed ledger system provides a great deal of transparency to all those who are a part of the network. Each node in a network has its own copy of the ledger and has the right to verify transactions. Due to this, no one can hide their details and transactions from the other users ensuring fair trade.

- Low transaction cost: As there are no intermediaries in a transaction within the blockchain network, the transaction costs are also lowered. Transactions of millions of dollars can happen for around $1.00 or even less. If there are intermediaries involved, then they charge a heavy amount and your overall transaction cost increases.

- Consensus-based: The blockchain concept is entirely consensus-based, that is, for every transaction that takes place between two nodes in a blockchain, a request for its verification is sent to all the other nodes. After all the nodes verify a transaction, it goes into the memory pool to make a new block. The memory pool stores numerous such verified transactions.

Enroll in Instructor-led Blockchain Certification Course to UPGRADE Your Skills

Weekday / Weekend BatchesSee Batch DetailsApplications of Blockchain

Now that we know what an ingenious technology blockchain is, it obviously finds its application in many fields and areas. In this section of the blockchain tutorial, we will discuss some of the most common fields which use blockchain technology.

- 1. Cloud Storage: Blockchain provides a decentralized system for storing files on the cloud. It is like an InterPlanetary File System (IPFS) in concept where sharing and storing files happen in a distributed web system rather than a client-server web which we currently have. Each website can act as a node which has a P2P transfer of files with other nodes directly, instead of requesting a central server.

- 2. Cryptocurrency: Blockchain technology acts as the backbone of cryptocurrency systems like Bitcoin. Cryptocurrency is an encrypted digital currency that everyone can use as a medium of exchange in transactions. Such transactions take place through the blockchain network. The blocks in a blockchain store the records related to generation and transaction of cryptocurrency between two nodes permanently. These days, there even exist cryptocurrency wallets where you can send and receive cryptocurrencies or exchange them for other currencies.

- 3. Healthcare: With the help of block-chaining, we can store information about patients and drugs in a database securely. Doctors can access patient records and history to analyze a case better at a given point to ensure proper treatment. Also, organizations can monitor and handle drug counterfeiting in the medical supply chain. This is because they can store the supply chain data as permanent blocks in the blockchain.

- 4. Smart Contracts: Ideally, when two parties sign an agreement or make a deal, it is a paper-based contract (which states all the terms and conditions of the deal) which the parties involved sign. However, this method of having deals and making contracts is subject to the risk of fraud and tampering. With blockchain as the base technology, a smart contract concept came into existence. Smart contracts are digital, self-executable contracts recorded and stored in a blockchain once created. A smart contract is a programmed file containing all the terms and conditions of a contract between two parties and it automatically executes itself once all the conditions are met. This gives a 100% guarantee and prevents the deal from any fraud.

Smart contracts were first introduced through an open-source blockchain network known as Ethereum. The smart contracts also find their application in areas like real estate property deals, financial agreements, insurances, crowdfunding, etc.

- Elections: Another interesting fact about blockchain is that we can participate in elections online with a blockchain system as its backbone guaranteeing the security of records and anonymity. People can cast vote online without physically showing up at a polling booth and the votes will be safely registered on a blockchain. It is nearly impossible for someone to hack into the system and tamper with the votes cast. This makes blockchain technology best for online voting as it would really increase the total number of people participating in elections.

- Digital Identity Management: With the digital revolution, the risks of fraud have also gone up significantly. More and more incidents of cybercrime and digital fraud are surfacing. This is due to easily hackable digital identities of people that hackers can use to do fraud and theft. To ensure the security of digital identities of people, blockchain is the best solution. Having the ids, passwords and authorized documents stored on blocks in a blockchain as a universal online directory. No fraud can occur as identity verification of every user is a necessary step in the blockchain system. One cannot access the online ledger if the credentials don’t match with the records of the blockchain network. Also, there is no chance of hacking in a blockchain system.

- Intellectual Property Protection: The information available on the internet is intellectual property. Nowadays, with enormous information getting shared on the internet, copyright issues are surfacing more than ever. Content is easily copied and distributed without the permission of the original author. However, there are copyright laws, but they are not quite in place. Moreover, there are no global laws or standards regarding copyrighting content which increases the problem.

Blockchain is again a savior here as one can copyright their content as a smart contract and store it in the blockchain. The authors or owners of the registered content will have full authority over the accessibility and distribution of their content and share it according to their will.

- 1. Automated Governance or DAOs: Automated governance or Decentralized Autonomous Organizations (DAOs) which are self-governed organizations. DAOs are self-governed organizations that abide by a strict set of rules. DAOs are built on blockchain and smart contracts as their foundations. Every stakeholder in a DAO will have equal authority and opportunity to contribute to the organization. This is unlike the traditional system where much of the corporate governance is under the control of the bureaucracy and hierarchical management.

- 2. Supply Chain Audits: Block-chaining also helps in guaranteeing the authenticity of a product in supply chain audits. Manufacturers can store the details of their products on a blockchain and consumers can verify the genuineness of the product by checking the records on the blockchain.

- 3. Sharing Economy: With blockchain, the need for intermediaries is gone and the trend of the direct transactions between interested parties has arrived. Apps like OpenBazaar use blockchain technology as they follow a peer-to-peer approach. Here, the seller uploads their product and quotes a suitable price. Then the interested buyer contacts the seller directly without an intermediary like Uber or Airbnb.

- 4. Internet of Things: As you all must be familiar with this term, IoT is our future! All the big players like IBM, AT&T, Samsung, etc. are focusing on enhancing their reach in the IoT market to become a global leader. Blockchain and smart contracts can prove to be useful for the implementation and workings of IoT systems. A smart contract can store software, sensors and other important details that will take care of the proper functioning of the electronic device and the network. Smart contracts execute themselves only when certain conditions are met properly and so it helps in monitoring and executing protocols for the IoT mechanisms using blockchain.

Bitcoin and Blockchain

Whenever you might have heard or read about blockchain, the word “Bitcoin” must have caught your attention. Bitcoin has become quite a popular phenomenon by now. So, what is bitcoin? Is it a physical coin?

Bitcoin is a digital cryptocurrency that is not a physical currency like a 10-rupee coin. Rather, it is a digital currency on a blockchain peer-to-peer network used in an encrypted form. Bitcoins transactions follow a distributed ledger system where transactions between two interested parties take place as a point-to-point exchange. Every node on the bitcoin blockchain verifies the bitcoin transaction and does proof-of-work (mining) to authorize the transaction and users. The transaction, upon getting verified, gets permanently added into an open blockchain as a new block. Bitcoins are also given as a reward to miners for doing correct proof-of-work in a blockchain network in order to add a new block in the chain. There will be a total of 21 million bitcoins created out of which 17 million are already in use. Blockchain was first used as the underlying technology of the Bitcoin system in 2009 when the Bitcoin ledger started on 3rd January 2009. We can exchange Bitcoins for other currencies, products or services by means of Bitcoin wallets available on the web.

Blockchain Case Study on Maersk

Before we conclude our introductory talk in the blockchain tutorial, let us go through a use case or case study of blockchain technology. This case study is about a famous Danish business conglomerate, Maersk.

Maersk is a business giant having operations in the areas of transport, logistics, and energy. Founded in 1904, it has continued to be one of the largest shipping and cargo service providers in the world.

The challenge:

The challenge facing Maersk was to keep a track of its shipments and manage the supply chain. Traditionally, such companies maintain all the records of consignments and shipments through the paperwork. But, any minor change in the shipment process would cause trouble as updating the paperwork will take time, delaying the shipment. Also, keeping the paperwork up to date in real-time with the shipments and supply chain activities was a tedious and meticulous task. All the stakeholders need proper, timely information on the shipments which was proving to be both time consuming and costly.

The solution:

Maersk came together with IBM and introduced a distributed platform where they can store records on a cloud-based database. It is like a private blockchain system where all the stakeholders involved can access real-time data in the supply chain ecosystem. This makes a global tamper-proof blockchain network that holds digitized information on trade and shipments. Anyone involved in the process can keep a track of the products shipped, cargo location, any detours or rerouting, etc. Thus, with the help of blockchain technology, Maersk was able to have a point-to-point secure network for data exchange and a tamper-proof repository to keep all the data/documents involved in the shipment process. This made the system more intact and safer, significantly avoiding any delays and frauds in the process. Also, the trade volume increased by 12% after implementing the new system.

Summary

This completes our introductory tutorial on blockchain technology. We hope we were able to give you a good basic understanding of this topic. Stay with us as we explore a lot of other domains where blockchain finds its application in the coming tutorials.