- Agile Sprint Planning | Everything You Need to Know

- What is Project Management Process ? : A Complete Guide

- What is Lean Management? : A Complete Guide

- What is ITIL ? Know about the Framework

- What is Six Sigma?| Know the tools used

- What is Kanban Training?|Know more about it

- Project Management Tools and Techniques : A Complete Guide

- What is Project Management? Everything You need to Know | Salary for the role

- Srum Org Certification? All you need to know about it

- MS Project Certification | All you need to know

- What is Project Manager? Know about the salary

- Six Sigma Certification Cost | Know all details about it

- Difference Between PMO and Project Manager? | Expert’s Top Picks

- What are Project Management Tools | Its Techniques | Everything You Need to Know

- What is Agile |Its Methodology and Types | How to Implement [ OverView ]

- What is a Product Roadmap? | How to Create one | A Complete Guide with Best Practices

- Scrum vs Kanban | Agile at Scale | New Agile BenchMark

- How to Effectively Manage Stakeholders | A Complete Guide For Beginners with Experts Top Picks

- What is Scaled Agile Framework (SAFe) | The Leading Framework For Business Agility | Everything You Need to Know

- How to Become a Project Manager | A Definitive Guide with Best Practices

- Time Management Tools to Help You Succeed as a Professional | Expert’s Top Picks

- Top 10 Tips for Agile Sprint Planning To Implement Efficient Marketing | Step-By-Step Process with REAL-TIME Examples

- What is ICP-ACC (ICAgile Certified Agile Coaching)? | A Definitive Guide with Best Practices [ OverView ]

- How To Run An Effective Agile Retrospective-Agile management | Everything You Need to Know

- What Skills Does One Acquire After The PMP Certification?

- A Definitive Guide: Most Effective and Proven Time Management Techniques [ OverView ]

- What Gaps I Filled After CSM Certification For my Scrum Project? [ OverView ]

- How to Create A Plan And Manage Your Projects Better?: Step-By-Step Process [ OverView ]

- What is User Story Mapping? : A Complete Guide with Best Practices

- What is Design Thinking ? : Benefits and Special Features | A Definitive Guide with Best Practices

- What is the Capability Maturity Model (CMM) [ For Freshers and Experience ]

- What is Sprint Planning ? | A Definitive Guide | Step-By-Step Process with REAL-TIME Examples

- What is Total Productive Maintenance (TPM) and How Does It Help in Equipment Effectiveness [ OverView ]

- What are Agile Metrics ? : A Complete Guide For Beginners [ OverView ]

- What is Agile Marketing and Why Do You Need It | Step-By-Step Process with REAL-TIME Examples

- Why is Retrospection Needed? : A Complete Guide For Beginners [ OverView ]

- Developing Project Schedule : Role of Float, Leads, and Lags [ OverView ]

- Project Life Cycle vs Product Life Cycle | Know Their Differences and Which Should You Learn?

- Projects in Business Environments | A Complete Guide For Beginners [ OverView ]

- What is Business Agility ? and Why is it Important ? Expert’s Top Picks

- The Most Important Benefits of Blended Learning | A Complete Guide For Beginners

- Can Business Analyst be a Project Manager? : Expert’s Top Picks

- Why A PMO Is Second In Line To A Project Manager ? | Expert’s Top Picks

- Devops vs Waterfall | A Definitive Guide and Which Should You Learn?

- Jira vs Trello | Know Their Differences and Which Should You Learn?

- Key Values and Principles Behind the Agile Manifesto | A Definitive Guide

- What are Scrum Ceremonies : The Ultimate Guide with Expert’s Top Picks

- Business Analyst vs Financial Analyst | Know Their Differences and Which Role is Better ?

- Learn Burndown Charts With Jira : Comprehensive Guide [ For Freshers and Experience ]

- What Is Scrum XP? : Step-By-Step Process with REAL-TIME Examples

- Phases of Project Management | Step-By-Step Process | Expert’s Top Picks

- Project Manager Salary in India – How much does a PM earn? [ Job & Future ]

- Why Do Scrum Masters Get Paid so Much? [For Freshers and Experience]

- What Best Describes a Scrum Team? All you need to know [ OverView ]

- JIRA vs TFS | Differences and Which Should You Learn?

- Anti-patterns of a Scrum Master : Step-By-Step Process

- SCM Tools and Frameworks | A Complete Guide with Best Practices

- Stages of Team Development | Everything You Need to Know

- Project Management Consultant : Job Description, Skills Required | Everything You Need to Know

- CSM vs PSM : Difference You Should Know

- Top Characteristics of a Project Manager : Expert’s Top Picks

- Roles And Responsibilities Of A Product Owner : Everything You Need to Know

- Common Project Risks and How to Tackle Them | Expert’s Top Picks

- Benefits of Having Shorter Sprints in Agile – Everything You Need to Know

- Group Discussion Tips | A Complete Guide with Best Practices

- PMP Certification Cost : All you need to know

- DMAIC Process and Methods | All you need to know [ OverView ]

- Agile Scrum Vs Kanban | Know the difference

- Deming vs Juran vs Crosby

- What is Project Scope Management and Why It’s Important?

- The Basic Principles of Project Management

- Top PMP Exam Questions and Answers for 2020

- Risk Management Strategies

- Roles and Responsibilities of A Scrum Master

- ROM Estimate Vs Definitive Estimate

- Guidelines for Creating and Maintaining a WBS Dictionary

- How to Become a Certified ScrumMaster?

- Top Professional Skills for 2020

- Fast Tracking Vs Crashing

- PMP Vs PRINCE2 Vs CAPM

- PMP Earned Value Management (EVM) And Formulas

- What is Certified Scrum Professional (CSM)?

- Top Leadership Theories Every Manager Should Know

- What is Deliverables in Project Management?

- How To Prepare For TOEFL

- History and evolution of the PMP Certification

- What Is Float In Microsoft Project?

- Rules to set you up for success in project

- What is Scrum Project Management?

- What Is Estimating Activity Duration in Project Management?

- What Are The PMP Terminologies Relating To Cost Knowledge Area?

- What is Project Scope Management processes?

- What Are The Types of Organization In PMP?

- Books to Beat the Scrum Master Certification

- Agile Coach Vs Agile Consultant

- What is the cost of quality in project management?

- Signs Your Career May Be Stagnation and Tips to Overcome Downturn

- Certified ScrumMaster (CSM) Certification

- Lean Six Sigma Black Belt Certification

- What is schedule Activity in project management?

- Why Do We Need a Project Charter?

- PMP Certification Exam Preparation Mind Map

- Why Quality Professionals Should Use Infographics In Project Management?

- Role of Earned Value Technique in Project Management

- What is Project Quality Management?

- Tools and Techniques to Estimate Project Cost

- What is a Project Charter And Project Scope in Project Management?

- Why Should You Conduct Project Status Meetings with Your Team?

- The 7 R’s of Change Management

- What Are The Categories and sources of risk in your project?

- What Is a Network Diagram in Project Management?

- What are The Types of Contracts In PMP?

- Residual Risk Vs Secondary Risk

- Impact of the stakeholders on the projects

- Effort Vs Duration Vs Elapsed Time

- Agile vs Scrum

- What Is Six Sigma Quality Assurance?

- How to Close a Project?

- What Qualifications Do You Need to be a Project Manager?

- Project Management Vs General Operations Management

- Enterprise Environmental Factors & Organizational Process Assets

- What is a project manager?

- Important Questions for PMP Certification Exam

- How is the PMP Exam changing, in 2015 & 2020?

- How To Renew Your PMP Certification?

- The Importance of Having Project Acceptance Criteria in Your Projects

- Tips for PMP Exam Preparation

- What is requirement traceability matrix RTM in Project Management?

- Poor Performance Appraisal? Here are the tips to turn any negative feedback into positive.

- How to build a successful Career in Agile and Scrum?

- Importance of Tuckman ladder model in HR management

- How To Apply For The PMP® Exam In Easy Steps

- How to Write a Six Sigma Problem Statement

- What is a lessons learned document in PMI?

- Perform Quality Assurance Vs Perform Quality Control

- How to Improve Quality Management Consistently?

- Interactive Vs Push Vs Pull Communication

- what is risk management?

- Key Appraisal Questions to Prepare For

- What are the MSP Certifications?

- What Is A Six Sigma Control Plan?

- How to Create a Project Plan in Excel?

- Agile Prioritization Techniques

- Tips to Help Millennials Climb the Corporate Ladder

- What is an Issue Log?

- Advantages of PMP over MBA

- Top Successful Project Estimation Techniques

- PMP Examination Preparation – ITTO’s

- Employee Training Rewards That Actually Improve Learning

- Lean principles

- What Does It Take to Become a Successful Agile Coach

- Projects VS Programs

- The Role of Six Sigma in Manufacturing

- The Top Formulas to Memorize Before Your PMP Exam

- Roadmap to CSM (Certified Scrum Master) Certification

- What are Some Qualities of a Good Manager and Good Leader?

- How to Handle Project Monitoring and Controlling Processes?

- Top Free Agile Tools For Any Project Manager

- Risk Assessment in Project Management

- The Concept of Zero Defects in Quality Management

- The Importance of Work Packages in Project Scope Management

- How to Get Project Management Experience for PMP Certification

- Different Ways to Calculate the Estimate at Completion (EAC)

- What Is a ScrumMaster?

- What is Risk Register?

- Agile Certifications

- Top-down Approach Vs Bottom-up Approach

- Leadership Vs Management

- What is Feasibility Study and Its Importance in Project Management?

- What Is a Project Management Plan?

- The Professional Advantages of the CAPM Certification

- PRINCE2 Vs PMP

- Rita Mulcahy’s PMP Prep and PMBOK® Guide

- What is Project Cycle Management?

- What is Project and Process Metrics?

- PMBOK® Sixth Edition is Here! What Project Managers Should Know?

- CAPM Certification

- Top Project Selection Methods for Project Managers

- Free Float Vs Total Float

- What is Critical Chain Project Management?

- How to Build a Career in Project Management?

- Scrum Master or Product Owner: What Suits You Better?

- Project Documentation and its Importance

- What is Performance Reporting in the Project Management?

- Top Highest Paying Tech Jobs in India

- Agile Sprint Planning | Everything You Need to Know

- What is Project Management Process ? : A Complete Guide

- What is Lean Management? : A Complete Guide

- What is ITIL ? Know about the Framework

- What is Six Sigma?| Know the tools used

- What is Kanban Training?|Know more about it

- Project Management Tools and Techniques : A Complete Guide

- What is Project Management? Everything You need to Know | Salary for the role

- Srum Org Certification? All you need to know about it

- MS Project Certification | All you need to know

- What is Project Manager? Know about the salary

- Six Sigma Certification Cost | Know all details about it

- Difference Between PMO and Project Manager? | Expert’s Top Picks

- What are Project Management Tools | Its Techniques | Everything You Need to Know

- What is Agile |Its Methodology and Types | How to Implement [ OverView ]

- What is a Product Roadmap? | How to Create one | A Complete Guide with Best Practices

- Scrum vs Kanban | Agile at Scale | New Agile BenchMark

- How to Effectively Manage Stakeholders | A Complete Guide For Beginners with Experts Top Picks

- What is Scaled Agile Framework (SAFe) | The Leading Framework For Business Agility | Everything You Need to Know

- How to Become a Project Manager | A Definitive Guide with Best Practices

- Time Management Tools to Help You Succeed as a Professional | Expert’s Top Picks

- Top 10 Tips for Agile Sprint Planning To Implement Efficient Marketing | Step-By-Step Process with REAL-TIME Examples

- What is ICP-ACC (ICAgile Certified Agile Coaching)? | A Definitive Guide with Best Practices [ OverView ]

- How To Run An Effective Agile Retrospective-Agile management | Everything You Need to Know

- What Skills Does One Acquire After The PMP Certification?

- A Definitive Guide: Most Effective and Proven Time Management Techniques [ OverView ]

- What Gaps I Filled After CSM Certification For my Scrum Project? [ OverView ]

- How to Create A Plan And Manage Your Projects Better?: Step-By-Step Process [ OverView ]

- What is User Story Mapping? : A Complete Guide with Best Practices

- What is Design Thinking ? : Benefits and Special Features | A Definitive Guide with Best Practices

- What is the Capability Maturity Model (CMM) [ For Freshers and Experience ]

- What is Sprint Planning ? | A Definitive Guide | Step-By-Step Process with REAL-TIME Examples

- What is Total Productive Maintenance (TPM) and How Does It Help in Equipment Effectiveness [ OverView ]

- What are Agile Metrics ? : A Complete Guide For Beginners [ OverView ]

- What is Agile Marketing and Why Do You Need It | Step-By-Step Process with REAL-TIME Examples

- Why is Retrospection Needed? : A Complete Guide For Beginners [ OverView ]

- Developing Project Schedule : Role of Float, Leads, and Lags [ OverView ]

- Project Life Cycle vs Product Life Cycle | Know Their Differences and Which Should You Learn?

- Projects in Business Environments | A Complete Guide For Beginners [ OverView ]

- What is Business Agility ? and Why is it Important ? Expert’s Top Picks

- The Most Important Benefits of Blended Learning | A Complete Guide For Beginners

- Can Business Analyst be a Project Manager? : Expert’s Top Picks

- Why A PMO Is Second In Line To A Project Manager ? | Expert’s Top Picks

- Devops vs Waterfall | A Definitive Guide and Which Should You Learn?

- Jira vs Trello | Know Their Differences and Which Should You Learn?

- Key Values and Principles Behind the Agile Manifesto | A Definitive Guide

- What are Scrum Ceremonies : The Ultimate Guide with Expert’s Top Picks

- Business Analyst vs Financial Analyst | Know Their Differences and Which Role is Better ?

- Learn Burndown Charts With Jira : Comprehensive Guide [ For Freshers and Experience ]

- What Is Scrum XP? : Step-By-Step Process with REAL-TIME Examples

- Phases of Project Management | Step-By-Step Process | Expert’s Top Picks

- Project Manager Salary in India – How much does a PM earn? [ Job & Future ]

- Why Do Scrum Masters Get Paid so Much? [For Freshers and Experience]

- What Best Describes a Scrum Team? All you need to know [ OverView ]

- JIRA vs TFS | Differences and Which Should You Learn?

- Anti-patterns of a Scrum Master : Step-By-Step Process

- SCM Tools and Frameworks | A Complete Guide with Best Practices

- Stages of Team Development | Everything You Need to Know

- Project Management Consultant : Job Description, Skills Required | Everything You Need to Know

- CSM vs PSM : Difference You Should Know

- Top Characteristics of a Project Manager : Expert’s Top Picks

- Roles And Responsibilities Of A Product Owner : Everything You Need to Know

- Common Project Risks and How to Tackle Them | Expert’s Top Picks

- Benefits of Having Shorter Sprints in Agile – Everything You Need to Know

- Group Discussion Tips | A Complete Guide with Best Practices

- PMP Certification Cost : All you need to know

- DMAIC Process and Methods | All you need to know [ OverView ]

- Agile Scrum Vs Kanban | Know the difference

- Deming vs Juran vs Crosby

- What is Project Scope Management and Why It’s Important?

- The Basic Principles of Project Management

- Top PMP Exam Questions and Answers for 2020

- Risk Management Strategies

- Roles and Responsibilities of A Scrum Master

- ROM Estimate Vs Definitive Estimate

- Guidelines for Creating and Maintaining a WBS Dictionary

- How to Become a Certified ScrumMaster?

- Top Professional Skills for 2020

- Fast Tracking Vs Crashing

- PMP Vs PRINCE2 Vs CAPM

- PMP Earned Value Management (EVM) And Formulas

- What is Certified Scrum Professional (CSM)?

- Top Leadership Theories Every Manager Should Know

- What is Deliverables in Project Management?

- How To Prepare For TOEFL

- History and evolution of the PMP Certification

- What Is Float In Microsoft Project?

- Rules to set you up for success in project

- What is Scrum Project Management?

- What Is Estimating Activity Duration in Project Management?

- What Are The PMP Terminologies Relating To Cost Knowledge Area?

- What is Project Scope Management processes?

- What Are The Types of Organization In PMP?

- Books to Beat the Scrum Master Certification

- Agile Coach Vs Agile Consultant

- What is the cost of quality in project management?

- Signs Your Career May Be Stagnation and Tips to Overcome Downturn

- Certified ScrumMaster (CSM) Certification

- Lean Six Sigma Black Belt Certification

- What is schedule Activity in project management?

- Why Do We Need a Project Charter?

- PMP Certification Exam Preparation Mind Map

- Why Quality Professionals Should Use Infographics In Project Management?

- Role of Earned Value Technique in Project Management

- What is Project Quality Management?

- Tools and Techniques to Estimate Project Cost

- What is a Project Charter And Project Scope in Project Management?

- Why Should You Conduct Project Status Meetings with Your Team?

- The 7 R’s of Change Management

- What Are The Categories and sources of risk in your project?

- What Is a Network Diagram in Project Management?

- What are The Types of Contracts In PMP?

- Residual Risk Vs Secondary Risk

- Impact of the stakeholders on the projects

- Effort Vs Duration Vs Elapsed Time

- Agile vs Scrum

- What Is Six Sigma Quality Assurance?

- How to Close a Project?

- What Qualifications Do You Need to be a Project Manager?

- Project Management Vs General Operations Management

- Enterprise Environmental Factors & Organizational Process Assets

- What is a project manager?

- Important Questions for PMP Certification Exam

- How is the PMP Exam changing, in 2015 & 2020?

- How To Renew Your PMP Certification?

- The Importance of Having Project Acceptance Criteria in Your Projects

- Tips for PMP Exam Preparation

- What is requirement traceability matrix RTM in Project Management?

- Poor Performance Appraisal? Here are the tips to turn any negative feedback into positive.

- How to build a successful Career in Agile and Scrum?

- Importance of Tuckman ladder model in HR management

- How To Apply For The PMP® Exam In Easy Steps

- How to Write a Six Sigma Problem Statement

- What is a lessons learned document in PMI?

- Perform Quality Assurance Vs Perform Quality Control

- How to Improve Quality Management Consistently?

- Interactive Vs Push Vs Pull Communication

- what is risk management?

- Key Appraisal Questions to Prepare For

- What are the MSP Certifications?

- What Is A Six Sigma Control Plan?

- How to Create a Project Plan in Excel?

- Agile Prioritization Techniques

- Tips to Help Millennials Climb the Corporate Ladder

- What is an Issue Log?

- Advantages of PMP over MBA

- Top Successful Project Estimation Techniques

- PMP Examination Preparation – ITTO’s

- Employee Training Rewards That Actually Improve Learning

- Lean principles

- What Does It Take to Become a Successful Agile Coach

- Projects VS Programs

- The Role of Six Sigma in Manufacturing

- The Top Formulas to Memorize Before Your PMP Exam

- Roadmap to CSM (Certified Scrum Master) Certification

- What are Some Qualities of a Good Manager and Good Leader?

- How to Handle Project Monitoring and Controlling Processes?

- Top Free Agile Tools For Any Project Manager

- Risk Assessment in Project Management

- The Concept of Zero Defects in Quality Management

- The Importance of Work Packages in Project Scope Management

- How to Get Project Management Experience for PMP Certification

- Different Ways to Calculate the Estimate at Completion (EAC)

- What Is a ScrumMaster?

- What is Risk Register?

- Agile Certifications

- Top-down Approach Vs Bottom-up Approach

- Leadership Vs Management

- What is Feasibility Study and Its Importance in Project Management?

- What Is a Project Management Plan?

- The Professional Advantages of the CAPM Certification

- PRINCE2 Vs PMP

- Rita Mulcahy’s PMP Prep and PMBOK® Guide

- What is Project Cycle Management?

- What is Project and Process Metrics?

- PMBOK® Sixth Edition is Here! What Project Managers Should Know?

- CAPM Certification

- Top Project Selection Methods for Project Managers

- Free Float Vs Total Float

- What is Critical Chain Project Management?

- How to Build a Career in Project Management?

- Scrum Master or Product Owner: What Suits You Better?

- Project Documentation and its Importance

- What is Performance Reporting in the Project Management?

- Top Highest Paying Tech Jobs in India

What Are The PMP Terminologies Relating To Cost Knowledge Area?

Last updated on 10th Oct 2020, Artciles, Blog, Project Management

It includes processes required to complete the project within the approved budget. With its processes, this knowledge area aims to determine the required budget to complete the project and then aims to monitor and control the project costs to meet the determined budget.

The major output of this knowledge area is Project Budget. After the project scope is clear and project activities are determined, each project deliverable and each project activity will have an associated cost. Because, project resources will perform activities, and they have some costs to projects such as expenses, salary etc. And there will be tools, materials or equipment that need to be used during the project as well. These will require a budget as well.

Subscribe For Free Demo

Error: Contact form not found.

This knowledge area primarily concerns the cost of resources needed to complete the project activities. After the budget is determined, cost management will keep on measuring and monitoring the cost performance of the project to meet the agreed budget.

Project Cost Management involves planning, budgeting, and managing costs. Cost management does not happen in isolation – the project manager needs input from the project team and key stakeholders. Cost management should occur early in project planning in order to establish a framework for all cost management processes and ensure that the project does not go over budget. In this PMP study material pdf, we’ll cover all the processes in the Cost Management Knowledge Area in PMBOK Guide 6th Edition PDF.

Although estimating cost and determining budgets can be one process on small projects, PMI separates them into two processes because the exam assumes the PM is managing a large project. Many financial management techniques, such as ROI, payback, and discounted cash flow, are used during this process.

Plan Cost Management

- 1.Plan Cost Management process establishes the framework/policies/procedures for how to estimate and manage costs

- 2.The key benefit of this process is that it provides guidance and direction on how costs are managed from project initiation to closure

- 3.There are many ways to fund a project, including: 1) Self-funding, 2) Funding with equity, or 3) Funding with debt

- 4.The Cost Management Plan is a component of the Project Management Plan that details how cost management processes will be carried out. This plan will describe how project costs are planned, estimated, and controlled.

- 5,The cost management plan also establishes the following:

-

- Units of measure

- Level of precision

- Level of accuracy

- Control thresholds

- Reporting formats

- Organizational procedures links

- Rules of performance measurement

- 6.Life Cycle Costing– Looking at the cost of the whole product life cycle, not just the cost on the project

- 7.Value Analysis– Finding less costly ways to do the same work. Value analysis involves identifying required project functions, assigning values to these functions, and providing these functions at the lowest cost without sacrificing performance.

Estimate Costs

- 1.Estimate Costs is the process of establishing an approximate monetary value to each project activity.

- 2.The key benefit of this process is that it determines the amount of money needed to complete project work

- 3.Cost estimate is a prediction of how much an activity will cost upon completion given the information we know now.

- 4.When estimating cost, you need to know whether you are only estimating the direct project costs or whether your estimates need to include indirect costs as well.

- 5.To estimate costs, you need to look at the project schedule to see which activities need which resources.

- 6.Types of Estimation:

-

- Analogous Estimating – use similar historical project activity costs to determine the current project activity costs. Relies of expert judgment. Use this technique when you have limited information available. Also called top-down estimating.

- Parametric Estimating – use mathematical calculations or models to determine activity costs (generally more accurate). E.g. it costs $100 to install 20m of wires, thus, it will cost $1000 to install 200m.

- Bottom-up Estimating – detailed estimating is done for each activity (if available) or work package (if activities are not defined), and the estimates are then rolled up into control accounts and finally into an over project estimate

- 7.Contingency Reserves – the part of the budget set aside to deal with negative risks that may occur

- 8.Vendor Bid Analysis – analyzing the bids from qualified vendors. If cost estimates vary significantly, it could mean that the scope is not well defined. If third-party vendors are used on the project, the PM needs to make sure their cost estimates are included in the project budget.

- 9.Activity cost estimate – an estimation of what the activity will cost upon completion based on information known to date.

- 10.Supporting details for activity cost estimates:

- Basis of estimation

- Assumptions

- Constraints

- Range of possible estimates

- Confidence level of final estimate

- 11.Types of costs:

- Variable costs – these costs change with the amount of production or the amount of work

-

- Examples: cost of material, supplies, and wages

- Fixed costs – these costs do not change as production changes

-

- Examples: rent, equipment, etc.

- Direct costs – these costs are directly attributable to the work on the project

- Examples are team travel, team wages, recognition, and costs of material used on the project

- Indirect costs – indirect costs are overhead items or costs incurred for the benefit of more than one project

-

- Examples include taxes, fringe benefits, and janitorial servicesCost of quality – The total cost of all efforts related to quality

Jump Start learning PMP Training & Enhance Your Skills

- Instructor-led Sessions

- Real-life Case Studies

- Assignments

- Accuracy of Estimates

Rough Order of Magnitude (ROM) Estimates

- This type of estimate is usually made during the initiating process

- A typical range from ROM estimate is a +/- 50% from actual, but this range can vary depending on how much is known about the project when creating the estimates

Budget estimate

- This type of estimate is usually made during the planning phase and is in the range of -10% to +25% from actual

Definitive estimate

- Later during the project, the estimate will become more refined. Some project managers use the range of +/- 10% from actual, while others use -5% to +10% from actual

Determine Budget

- 1.Determine Budget is the process of aggregating individual activity or work package costs into the project budget.

- 2.The Key Benefit of this process is that it determines the cost baseline against which project performance is measured.

- 3.Cost aggregation– the process of rolling up individual activity costs into work packages and work packages into control accounts and control accounts into the project budget

- 4.Funding limit reconciliation – Comparing plan project expenditures against funding limits to determine if any variances exist.

- 5.Cost baseline– approved time-phased project budget. The cost baseline tells you how much you should have spent at any given point in time. Any changes to the cost baseline must be approved by the change control board.

- 6.Control accounts– During reporting, the key stakeholders may want more details than the overall project cost, but less details than the work packages costs. Control accounts aggregates related work packages together. The PM will report at the control accounts level.

- 7.Reserve analysis:

- 8.Management reserves

-

- “Unknown-unknown risks”

- Not part of the project baseline

- Sponsor must approve the use of management reserves and then the project must be “re-baselined”

- Contingency reserves

- “known-unknown risks”

- Used at the discretion of the project manager

- Part of the project budget

- The summation of control accounts gives you your cost baseline.

- Cost baseline + contingency reserves = project budget

- Funding occurs in incremental stages that are not continuous or evenly distributed.

- Funding requirements are derived from the cost baseline

Control Costs

- The Control Costs process is the process of monitoring actual project costs against the cost baseline and managing changes to the cost baseline.

- The key benefit of this process is that it allows the PM to detect cost variances early and take corrective actions to bring the project back on budget.

- Any changes to the budget must be approved through the Perform Integrated Change Control process.

- Project Cost Control components:

- Ensuring timely implementation of change requests

- Issuing cost-related change requests when necessary

- Monitoring cost performance and understanding the root causes of variances

- Monitoring activity costs against project budget

- Reporting cost performances to key stakeholders

- Ensuring the project do not exceed funding limits

- Preventing unapproved changes from using up the budget

- Bringing cost overruns to within acceptable limits

- Variance analysis – The procedure of analyzing the difference between the actual cost and the budgeted cost (from the cost baseline).

- Return on investment (ROI) – a technique to estimate the potential profitability of an investment

- Progress Reporting

- 1.50/50 rule

- An activity is considered 50% complete when it begins and gets credit for the last 50% only when it is completed

- 2.20/80 rule

- An activity is considered 20% complete when it begins and get credit for the last 80% only when it is completed

- 3.1/100 rule

- An activity does not get credit for partial completion. It only gets credit for full completion

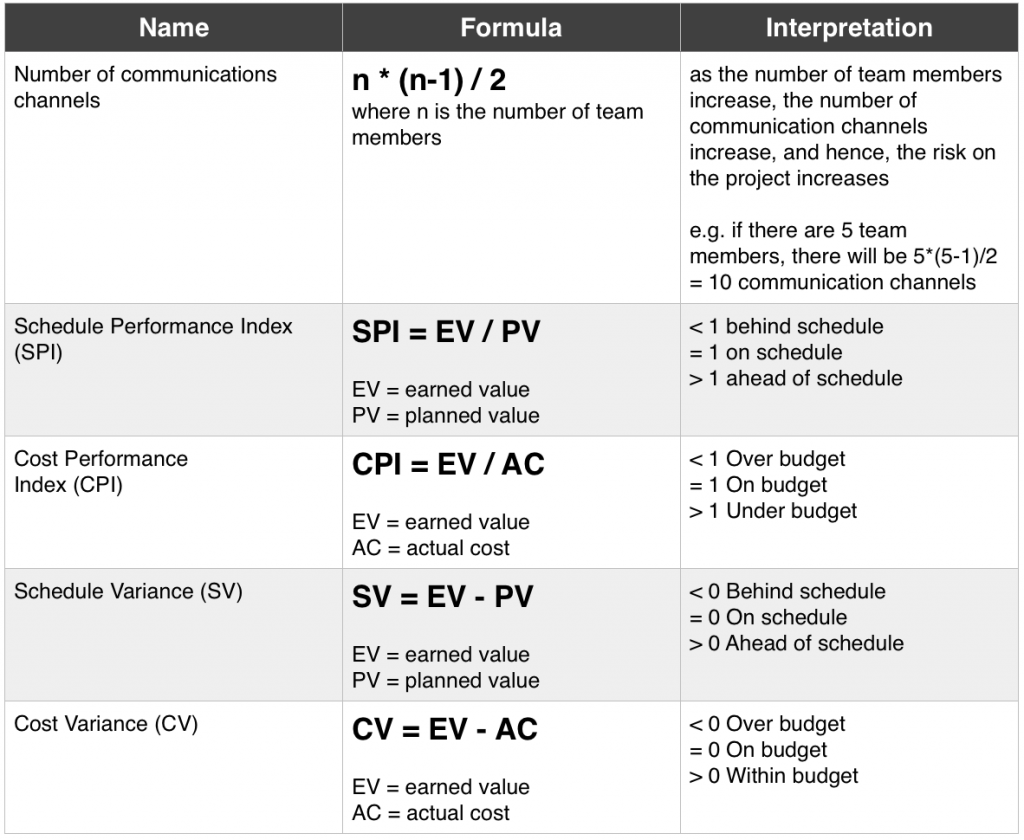

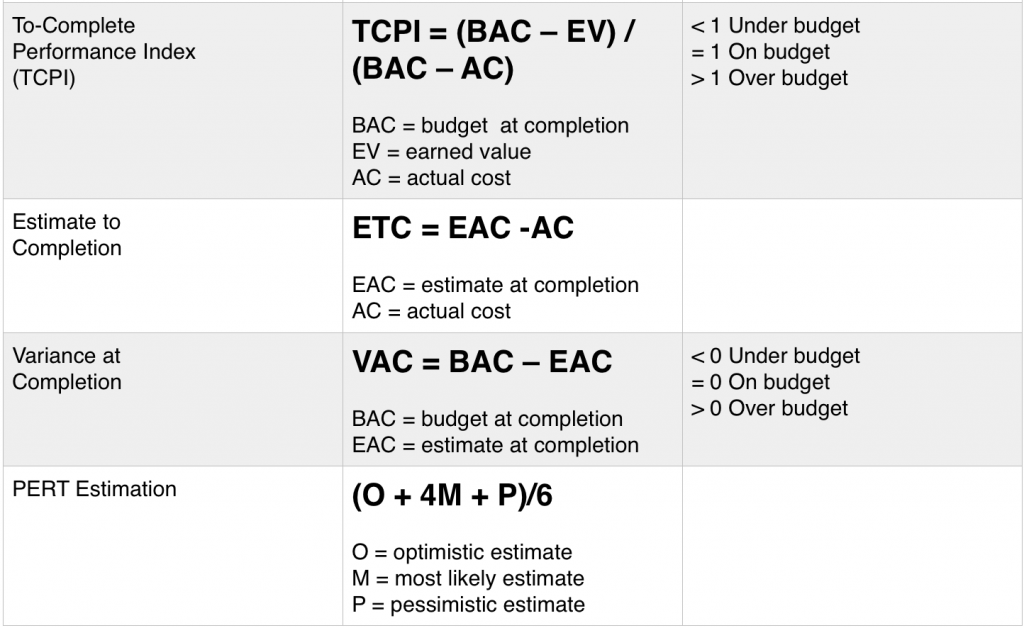

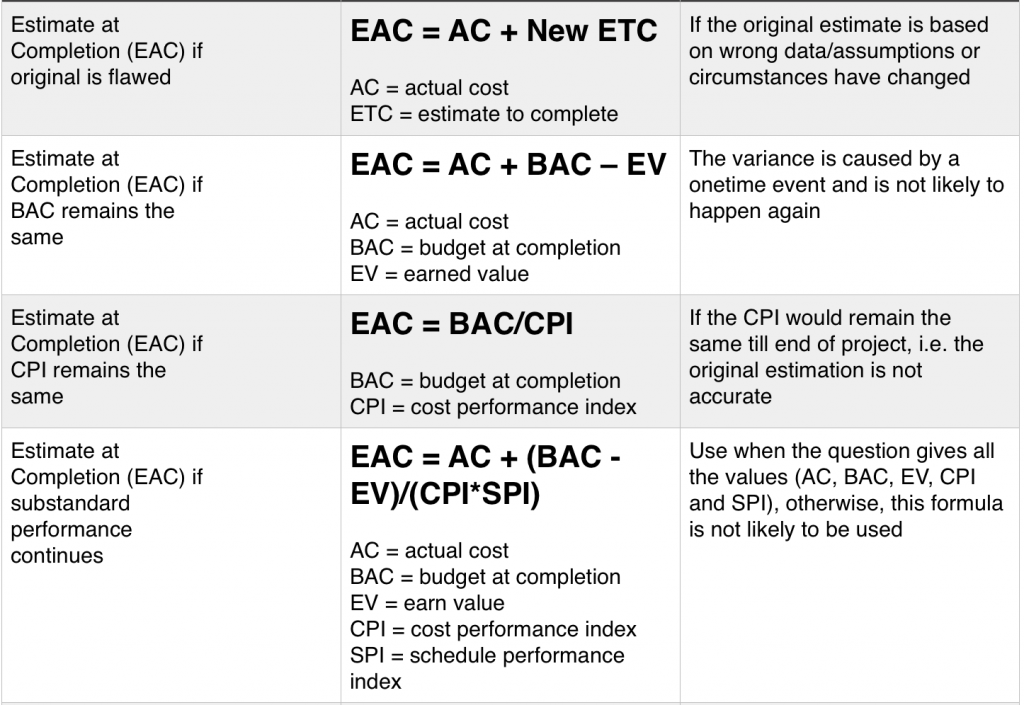

- Earned Value Management – This methodology is used to measure project performance against the scope, schedule, and cost baselines.

| Acronym | Term | Interpretations |

|---|---|---|

| PV | Planned value | As of today, what is the estimate value of the work planned to be done? |

| EV | Earned value | As of today, what is the estimated value of the work actually accomplished? |

| AC | Actual cost (total cost) | As of today, what is the actual cost incurred for the work accomplished? |

| BAC | Budget at completion | How much did we BUDGET for the TOTAL project effort? |

| EAC | Estimate at completion | What do we currently expect the TOTAL project to cost (a forecast)? |

| ETC | Estimate to complete | From this point on, how much more do we expect it to cost to finish |

| VAC | Variance at completion | As of today, how much over or under budget do we expect to be at the end of the project? |